Getting Started with NNS: Sampling and Simulation

Fred Viole

Source:vignettes/NNSvignette_Sampling.Rmd

NNSvignette_Sampling.RmdNNS offers several novel sampling methods from any

distribution, as well as simulating variables while maintaining their

dependence.

Sampling

CDFs

Cumulative distribution functions (CDFs) represent the probability a variable will take a value less than or equal to .

Empirical CDF

The empirical CDF is a simple construct, provided in the base package

of R. We can generate an empirical CDF with the ecdf

function and create a function (P) to return the CDF of a

given value of

.

## Empirical CDF

## Call: ecdf(x)

## x[1:100] = -2.3092, -1.9666, -1.6867, ..., 2.169, 2.1873

P = ecdf(x)

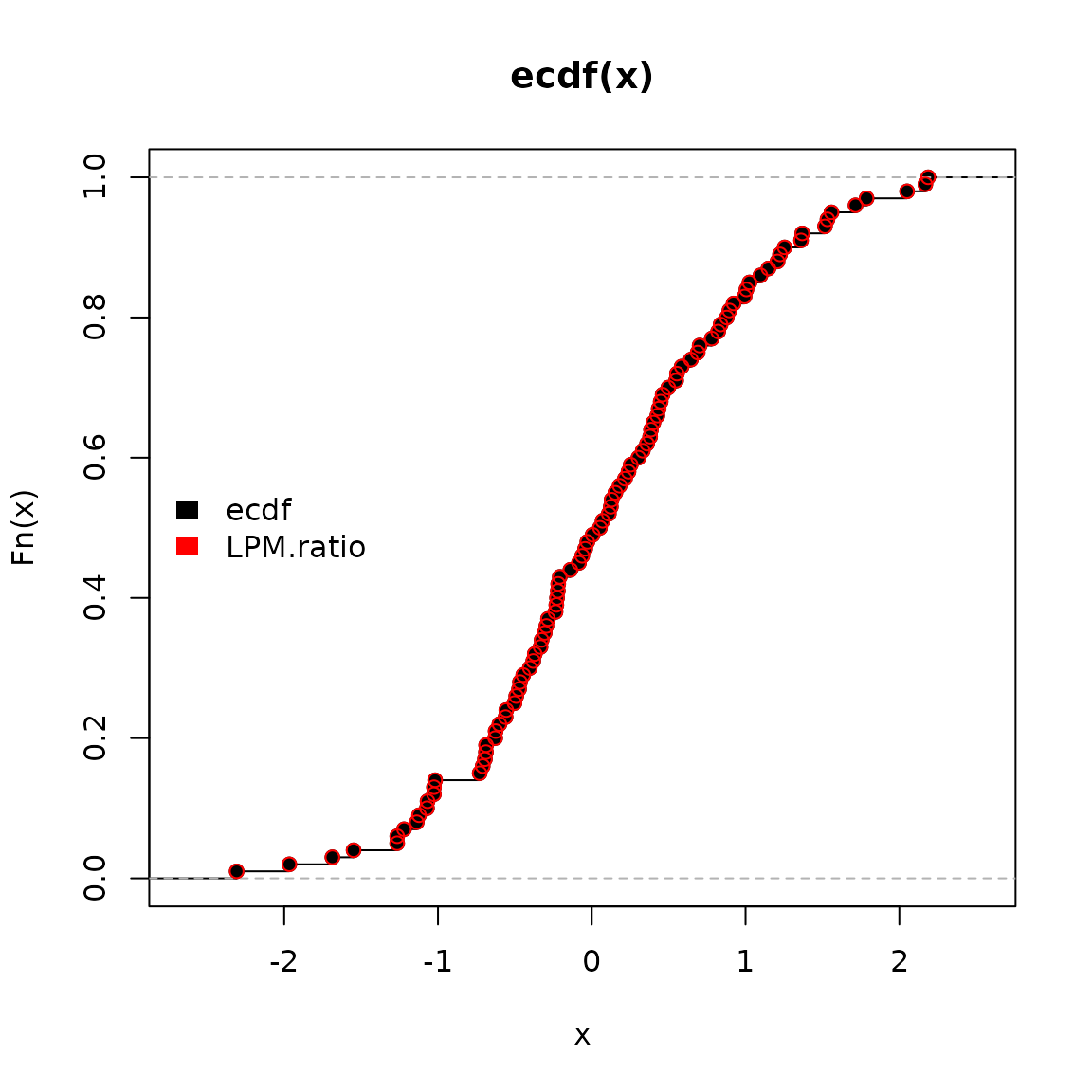

P(0); P(1)## [1] 0.48## [1] 0.83Lower Partial Moment CDF

(LPM.ratio)

The empirical CDF and Lower Partial Moment CDF

(LPM.ratio) are identical when the degree

term of the LPM.ratio is set to zero.

Degree 0 LPM:

LPM.ratio is equivalent to the following form for any

target

and variable

:

Using the same targets from our ecdf example above (0,1)

we can compare LPM.ratios.

## [1] 0.48## [1] 0.83Calculating the probability for every target value in

,

we can plot both methods visualizing their identical results.

ecdf function in black and

LPM.ratio in red.

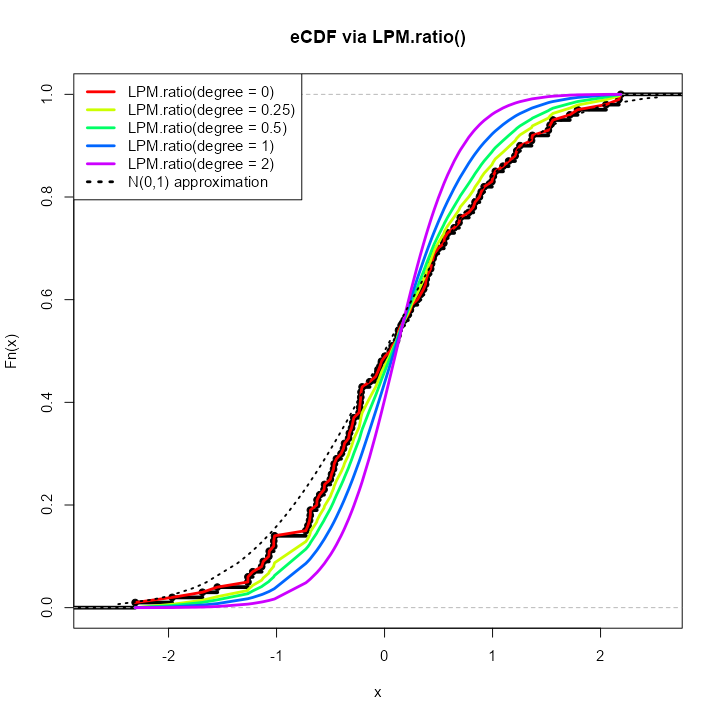

LPM.ratio degree > 0

By simply increasing the degree parameter to any

positive real number, we can generate different CDFs of our initial

distribution

.

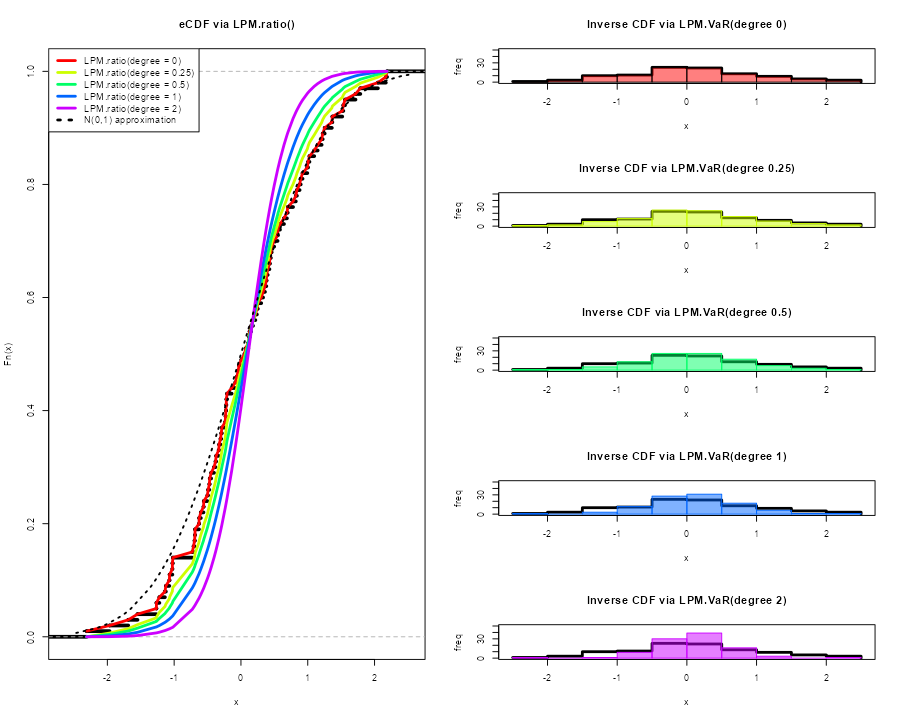

Generating PDFs with (LPM.VaR)

We can now generate distributions using the same insights and

degree manipulation in the corresponding

LPM.VaR function, a la value-at-risk,

providing inverse CDF estimates.

The general form in the following plots is:

LPM.VaR(percentile = seq(0, 1, length.out = 100), degree = 0, x = x)

Any length percentile can be used to sample from the

underlying distribution

.

Viewing the first 10 samples from each of the degrees

compared to our original

.

degree.0.samples = LPM.VaR(percentile = seq(0, 1, length.out = 100), degree = 0, x = x)

degree.0.25.samples = LPM.VaR(percentile = seq(0, 1, length.out = 100), degree = 0.25, x = x)

degree.0.5.samples = LPM.VaR(percentile = seq(0, 1, length.out = 100), degree = 0.5, x = x)

degree.1.samples = LPM.VaR(percentile = seq(0, 1, length.out = 100), degree = 1, x = x)

degree.2.samples = LPM.VaR(percentile = seq(0, 1, length.out = 100), degree = 2, x = x)

head(data.table::data.table(cbind("original x" = sort(x), degree.0.samples,

degree.0.25.samples,

degree.0.5.samples,

degree.1.samples,

degree.2.samples)), 10)

original x degree.0.samples degree.0.25.samples degree.0.5.samples

1: -2.309169 -2.309169 -2.309097 -2.3090915

2: -1.966617 -1.966617 -1.941190 -1.6935509

3: -1.686693 -1.686693 -1.599486 -1.4541494

4: -1.548753 -1.548753 -1.382553 -1.2462731

5: -1.265396 -1.265396 -1.250823 -1.1453748

6: -1.265061 -1.265061 -1.176436 -1.0745440

7: -1.220718 -1.220718 -1.119655 -1.0252742

8: -1.138137 -1.138137 -1.067793 -0.9868693

9: -1.123109 -1.123109 -1.026429 -0.9322105

10: -1.071791 -1.071791 -1.014276 -0.8710942

degree.1.samples degree.2.samples

1: -2.3091021 -2.3091170

2: -1.4744653 -1.1614908

3: -1.2159961 -0.9709972

4: -1.0823023 -0.8610192

5: -0.9968028 -0.7810300

6: -0.9290505 -0.7169770

7: -0.8666886 -0.6631888

8: -0.8090433 -0.6170691

9: -0.7556644 -0.5765608

10: -0.7069835 -0.5403318Simulation

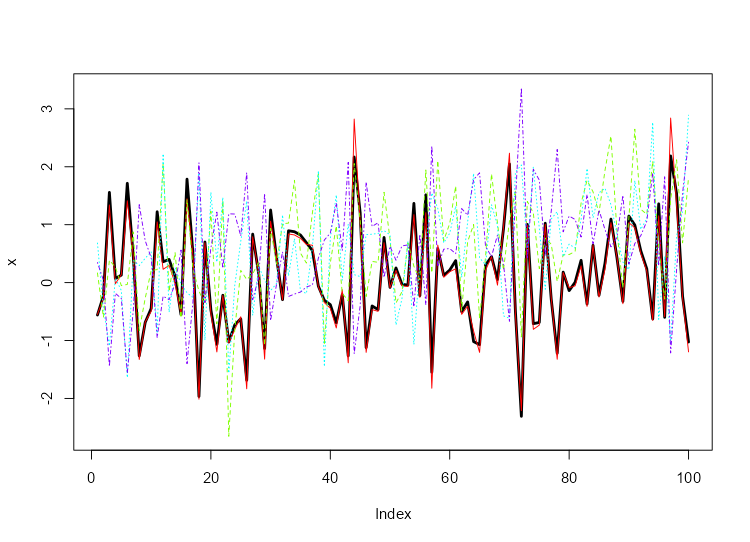

Bootstrapping (NNS.meboot)

NNS.meboot is based on the maximum

entropy bootstrap, available in the R-package meboot. This

procedure is specifically designed for time-series and avoids the IID

assumption in traditional methods.

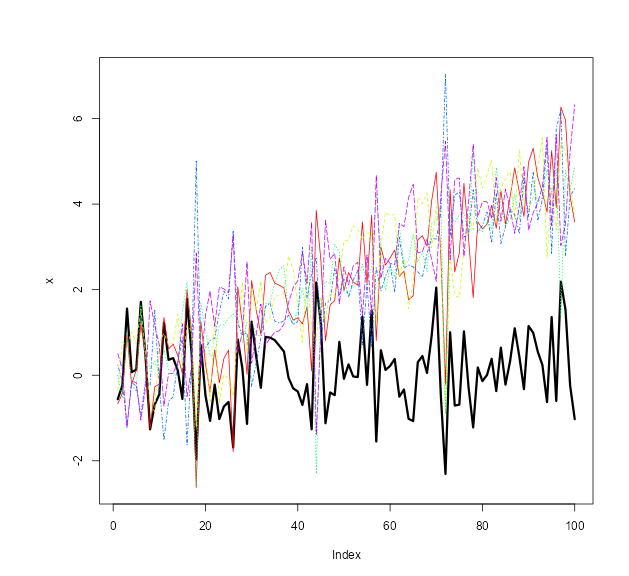

The ability to sample from specified correlations ensures the full spectrum of future paths is sampled from. Typical Monte Carlo samples are restricted to [-0.3, 0.3] correlations to the original data.

We will generate 1 replicate of

for each value of a sequence of

values (the

),

and then plot the results compared to our original

(black line). NNS.MC is a streamlined

wrapper function for this functionality of

NNS.meboot.

boots = NNS.MC(x, reps = 1, lower_rho = -1, upper_rho = 1, by = .5)$replicates

reps = do.call(cbind, boots)

matplot(reps, type = "l", col = rainbow(length(boots)))

lines(x, type = "l", lwd = 3, ylim = c(min(reps), max(reps)))

Checking our replicate correlations:

sapply(boots, function(r) cor(r, x, method = "spearman"))

rho = 1 rho = 0.5 rho = 0 rho = -0.5 rho = -1

0.99732373 0.51147915 0.01036904 -0.48720072 -0.98294629 More replicates and ensembles thereof can be generated for any number of values.

target_drift Specification

We can also specify a target drift in our replicates with the

target_drift parameter.

boots = NNS.MC(x, reps = 1, lower_rho = -1, upper_rho = 1, by = .5, target_drift = 0.05)$replicates

reps = do.call(cbind, boots)

plot(x, type = "l", lwd = 3, ylim = c(min(c(x, reps)), max(c(x, reps))))

matplot(reps, type = "l", col = rainbow(length(boots)), add = TRUE)

Please see the full NNS.meboot and

NNS.MC argument documentation.

Simulating a Multivariate Dependence Structure

Analogous to an empirical copula transformation, we can generate

new data from the dependence structure of our

original data via the following steps:

- Determine the dependence structure:

This is accomplished using

LPM.ratio(1, x, x) for continuous

variables, and LPM.ratio(0, x, x) for

discrete variables, which are the empirical CDFs of the marginal

variables.

- Generate or supply

new data:

new data does not have to be of the same distribution or

dimension as the original data, nor does each dimension of

new data have to share a distribution type.

- Apply dependence structure to

new data:

We then utilize LPM.VaR to ascertain

new data values corresponding to original data

position mappings, and return a matrix of these transformed values with

the same dimensions as new.data.

set.seed(123)

x = rnorm(1000); y = rnorm(1000); z = rnorm(1000)

# Add variable x to original data to avoid total independence (example only)

original.data = cbind(x, y, z, x)

# Determine dependence structure

dep.structure = apply(original.data, 2, function(x) LPM.ratio(degree = 1, target = x, variable = x))

# Generate new data with different mean, sd and length (or distribution type)

new.data = sapply(1:ncol(original.data), function(x) rnorm(nrow(original.data)*2, mean = 10, sd = 20))

# Apply dependence structure to new data

new.dep.data = sapply(1:ncol(original.data), function(x) LPM.VaR(percentile = dep.structure[,x], degree = 1, x = new.data[,x]))Compare Multivariate Dependence Structures

Similar dependence with radically different values, since we used in place of our original observations.

head(original.data)

head(new.dep.data)

x y z x

[1,] -0.56047565 -0.99579872 -0.5116037 -0.56047565

[2,] -0.23017749 -1.03995504 0.2369379 -0.23017749

[3,] 1.55870831 -0.01798024 -0.5415892 1.55870831

[4,] 0.07050839 -0.13217513 1.2192276 0.07050839

[5,] 0.12928774 -2.54934277 0.1741359 0.12928774

[6,] 1.71506499 1.04057346 -0.6152683 1.71506499

[,1] [,2] [,3] [,4]

[1,] -2.028109 -10.498044 -0.2090467 -1.682949

[2,] 4.608303 -11.390485 15.6213689 4.852534

[3,] 39.478741 8.836581 -0.8508203 40.585505

[4,] 10.683731 6.609255 36.0328589 10.877677

[5,] 11.866922 -47.955235 14.3111350 12.064633

[6,] 42.665726 29.639640 -2.4141874 43.797025Alternative Using NNS.meboot

Alternatively, if we wish to keep the simulated values close to the

original data, we can apply the NNS.meboot

procedure to each of the variables.

We will generate 1 replicate (for brevity) of

to our original.data, use their ensemble and

note the multivariate dependence among our

new.boot.dep.data.

# Apply bootstrap to each variable

new.boot.dep.data = apply(original.data, 2, function(r) NNS.meboot(r, reps = 100, rho = .95))

# Reformat into vectors

boot.ensemble.vectors = lapply(new.boot.dep.data, function(z) unlist(z["ensemble",]))

# Create matrix from vectors

new.boot.dep.matrix = do.call(cbind, boot.ensemble.vectors)Checking ensemble correlations with

original.data:

for(i in 1:4) print(cor(new.boot.dep.matrix[,i], original.data[,i], method = "spearman"))

[1] 0.9452863

[1] 0.9499478

[1] 0.945878

[1] 0.9442845Compare Multivariate Dependence Structures

Similar dependence with similar values.

head(original.data)

head(new.boot.dep.matrix)

x y z x

[1,] -0.56047565 -0.99579872 -0.5116037 -0.56047565

[2,] -0.23017749 -1.03995504 0.2369379 -0.23017749

[3,] 1.55870831 -0.01798024 -0.5415892 1.55870831

[4,] 0.07050839 -0.13217513 1.2192276 0.07050839

[5,] 0.12928774 -2.54934277 0.1741359 0.12928774

[6,] 1.71506499 1.04057346 -0.6152683 1.71506499

x y z x

ensemble1 -0.4268047 -0.7794553 -0.6364458 -0.4642642

ensemble2 -0.2965744 -1.0682197 0.3297265 -0.2531178

ensemble3 1.3302149 0.3054734 -0.4014515 1.4914884

ensemble4 0.2257378 0.3108846 1.0603892 0.1728540

ensemble5 0.4716743 -3.3344967 -0.1917697 0.4309379

ensemble6 1.3984978 1.1881374 -0.5295386 1.5326055References

If the user is so motivated, detailed arguments and proofs are provided within the following: