Getting Started with NNS: Normalization and Rescaling

Fred Viole

Source:vignettes/NNSvignette_Normalization_and_Rescaling.Rmd

NNSvignette_Normalization_and_Rescaling.RmdOverview

This vignette covers two related tools:

-

NNS.norm()for cross‑variable normalization when comparing multiple series. -

NNS.rescale()for single‑vector rescaling with either min‑max or risk‑neutral targets.

Both functions perform deterministic affine transformations that preserve rank structure while modifying scale.

NNS.norm(): Normalize Multiple Variables

NNS.norm() rescales variables to a common magnitude

while preserving distributional structure. The method can be

linear (all variables forced to have the same mean) or

nonlinear (using dependence weights to produce a more

nuanced scaling). In the nonlinear case, the degree of association

between variables influences the final normalized values.

Mathematical Structure

Let be an matrix of variables.

Step 3: Dependence Weight Matrix

If linear = FALSE:

- If number of variables :

- Otherwise:

NNS.dep()returns a symmetric matrix of nonlinear dependence measures.

If linear = TRUE, the weighting effectively becomes:

Nonlinear Case Interpretation

Thus, the normalized mean becomes a dependence‑weighted average of original means. Variables more strongly dependent with higher‑mean variables scale upward more.

Examples

Basic Multivariate Example

This holds for any distribution type and can be applied to vectors of different lengths.

set.seed(123)

A <- rnorm(100, mean = 0, sd = 1)

B <- rnorm(100, mean = 0, sd = 5)

C <- rnorm(100, mean = 10, sd = 1)

D <- rnorm(100, mean = 10, sd = 10)

X <- data.frame(A, B, C, D)

# Linear scaling

lin_norm <- NNS.norm(X, linear = TRUE, chart.type = NULL)

head(lin_norm)

A Normalized B Normalized C Normalized D Normalized

[1,] -29.929719 31.889828 5.819152 1.4264014

[2,] -12.291609 -11.531393 5.396317 1.2388239

[3,] 83.235911 11.073887 4.643781 0.3078703

[4,] 3.765188 15.601030 5.029380 -0.2630481

[5,] 6.904039 42.717726 4.572611 2.8193657

[6,] 91.585447 2.021274 4.543080 6.6681079

# Verify means are equal

apply(lin_norm, 2, function(x) c(mean = mean(x), sd = sd(x)))

A Normalized B Normalized C Normalized D Normalized

mean 4.827727 4.827727 4.8277270 4.827727

sd 48.744888 43.407590 0.4531172 5.203436Now compare with nonlinear scaling:

nonlin_norm <- NNS.norm(X, linear = FALSE, chart.type = NULL)

head(nonlin_norm)

A Normalized B Normalized C Normalized D Normalized

[1,] -2.7834653 0.32807768 3.178568 0.7439872

[2,] -1.1431202 -0.11863321 2.947605 0.6461499

[3,] 7.7409438 0.11392645 2.536550 0.1605800

[4,] 0.3501627 0.16050101 2.747174 -0.1372015

[5,] 0.6420759 0.43947344 2.497676 1.4705341

[6,] 8.5174510 0.02079456 2.481545 3.4779738

apply(nonlin_norm, 2, function(x) c(mean = mean(x), sd = sd(x)))

A Normalized B Normalized C Normalized D Normalized

mean 0.4489788 0.04966692 2.637026 2.518062

sd 4.5332769 0.44657066 0.247504 2.714025Note that the means differ and the standard deviations are smaller than in the linear case, reflecting the dependence structure.

Normalize list of unequal vector lengths

set.seed(123)

vec1 <- rnorm(n = 10, mean = 0, sd = 1)

vec2 <- rnorm(n = 5, mean = 5, sd = 5)

vec3 <- rnorm(n = 8, mean = 10, sd = 10)

vec_list <- list(vec1, vec2, vec3)

NNS.norm(vec_list)

$`x_1 Normalized`

[1] 13.074058 -3.004912 -11.745878 25.406891 -4.647966 -5.481229 6.225165 5.920719 6.113733 9.640242

$`x_2 Normalized`

[1] 2.875960212 0.008876158 1.230826150 5.855582361 10.779166523

$`x_3 Normalized`

[1] 4.0749062 2.2395840 0.4067264 0.7457562 15.6445780 5.1941416 2.3326665 2.5622994Quantile Normalization Comparison

Quantile normalization forces distributions to be identical. This is

literally the opposite intended effect of NNS.norm, which

preserves individual distribution shapes while aligning ranges. The

quantile normalized series become identical in distribution, while the

NNS methods retain the original patterns.

Practical Applications

Normalization eliminates the need for multiple y‑axis charts and

prevents their misuse. By placing variables on the same axes with shared

ranges, we enable more relevant conditional probability analyses. This

technique, combined with time normalization, is used in

NNS.caus() to identify causal relationships between

variables.

NNS.rescale(): Distribution Rescaling

NNS.rescale() performs one‑dimensional affine

transformations.

Function signature:

NNS.rescale(x, a, b, method = "minmax", T = NULL, type = "Terminal")1) Min-Max Scaling

If method = "minmax":

Properties:

- Preserves order

- Maps support to

- Linear transformation

Example

raw_vals <- c(-2.5, 0.2, 1.1, 3.7, 5.0)

scaled_minmax <- NNS.rescale(

x = raw_vals,

a = 5,

b = 10,

method = "minmax",

T = NULL,

type = "Terminal"

)

cbind(raw_vals, scaled_minmax)

#> raw_vals scaled_minmax

#> [1,] -2.5 5.000000

#> [2,] 0.2 6.800000

#> [3,] 1.1 7.400000

#> [4,] 3.7 9.133333

#> [5,] 5.0 10.000000

range(scaled_minmax)

#> [1] 5 10Risk-Neutral Example

set.seed(123)

S0 <- 100

r <- 0.05

T <- 1

# Simulate a price path

prices <- S0 * exp(cumsum(rnorm(250, 0.0005, 0.02)))

rn_terminal <- NNS.rescale(

x = prices,

a = S0,

b = r,

method = "riskneutral",

T = T,

type = "Terminal"

)

c(

mean_original = mean(prices),

mean_rescaled = mean(rn_terminal),

target = S0 * exp(r * T)

)

mean_original mean_rescaled target

109.7019 105.1271 105.1271 Conceptual Summary

NNS.norm()

- Multivariate

- Dependence‑aware scaling

- Equalizes means only in linear mode

- Preserves shape and order

NNS.rescale()

- Univariate

- Affine transformation

- Either range‑targeted or expectation‑targeted

- Preserves rank structure

Both functions maintain monotonicity and are therefore compatible with NNS copula and dependence modeling frameworks.

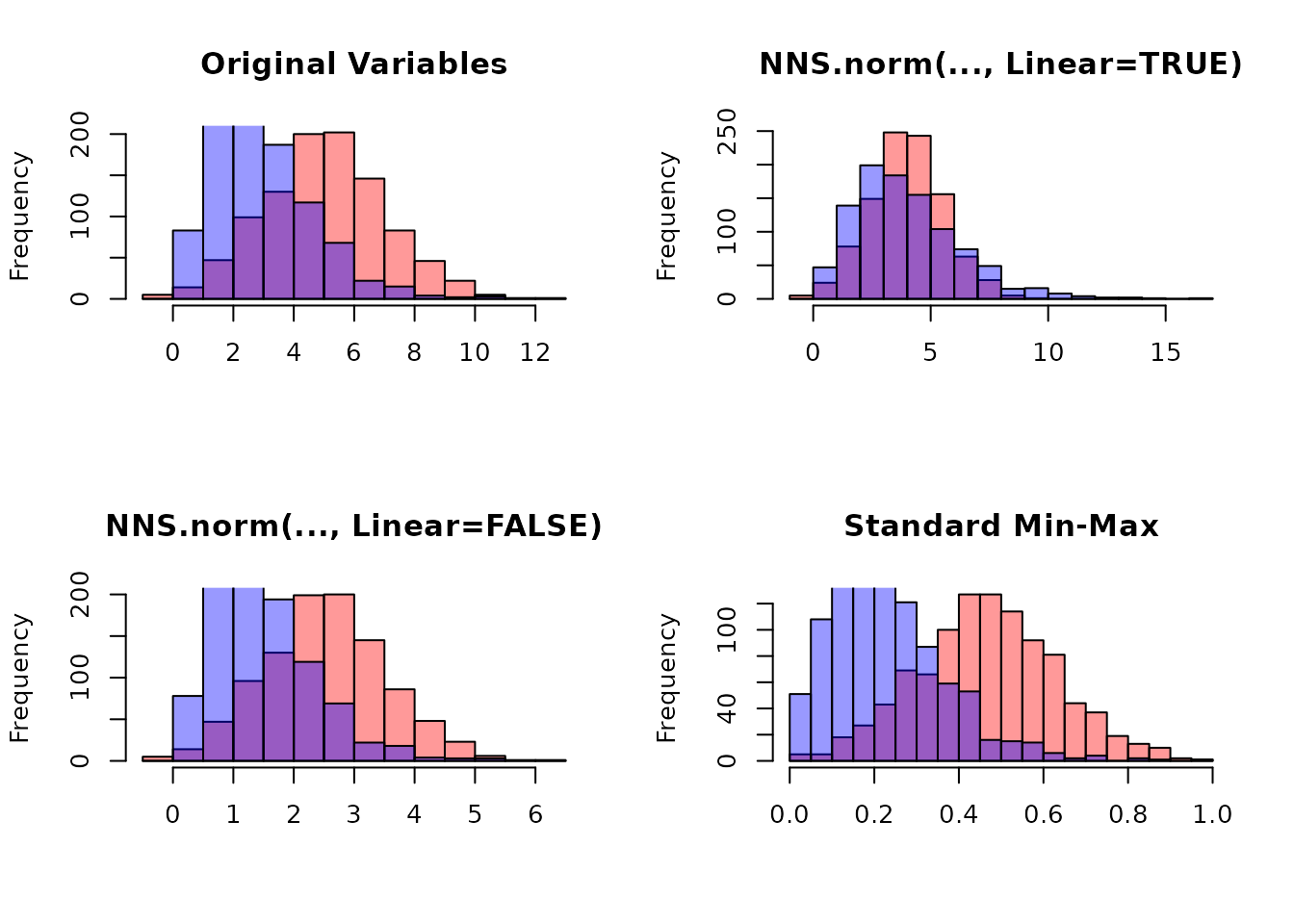

set.seed(123)

x <- rnorm(1000, 5, 2)

y <- rgamma(1000, 3, 1)

# Combine variables

X <- cbind(x, y)

# NNS normalization

X_norm_lin <- NNS.norm(X, linear = TRUE)

X_norm_nonlin <- NNS.norm(X, linear = FALSE)

# Standard min-max normalization

minmax <- function(v) (v - min(v)) / (max(v) - min(v))

X_minmax <- apply(X, 2, minmax)